Insurance is probably one of the most complex yet also critically important topics amongst young Singaporean adults. In recent years, I have had so many conversations with friends and even strangers on what insurance policies to buy and why, that I think a blog post on this topic is long overdue.

Caveat: I am not an insurance agent, just someone who read up on the topic and consulted many agents from the different companies to compare and rationalized what is best for my own interests. And I recommend everyone do the same too instead of relying on one friend or one source of information.

This isn’t the most straightforward of topics so I’ll try to break it down as simply as possible in 3 SIMPLE POINTS:

1) What is the point of insurance?

A lot of people lose the plot when they meet agents who try to up sell them with insurance products that have one and a million features. Hence it’s critical to go back to the basics and understand what is the point of insurance in the first place.

In simple terms: Getting through life is risky business because many bad things can happen. However because risk is something quantifiable (RISK = frequency of bad thing happening x impact on you/family if bad thing happens), insurance companies help to manage the risk by transferring cost of significant potential loss to themselves in exchange for money (which we pay them as premiums) across large numbers of clients .

There are many risks in life in general, but there is no need to get insurance to cover for every possible scenario in life (unless you have plenty of money to throw away).

Ideally you buy insurance for scenarios that will have a big impact on you/family if it happens AND you believe you will need additional financing during that scenario –but definitely NOT anything and everything that your agent suggests (especially investment-link plans).

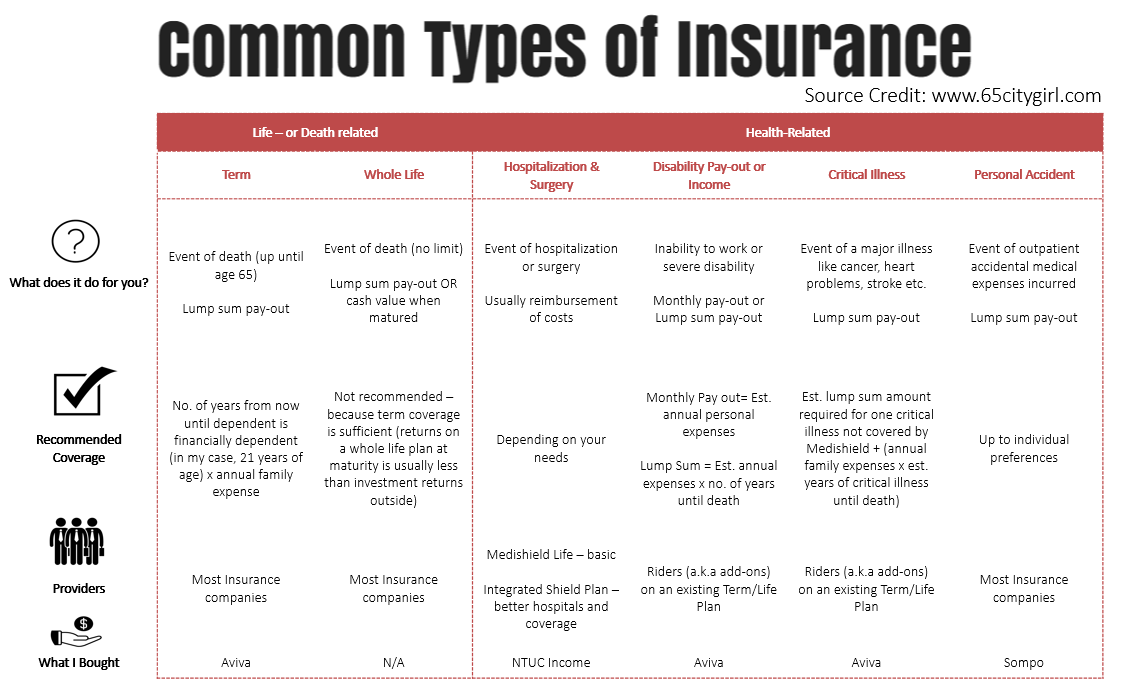

2) What are the common types of insurance available?

Additional things to take note of when speaking to your agent about your needs:

- Use EXPENSES to calculate coverage instead of INCOME otherwise you would be over-paying for your premiums

- Remind them to help adjust all recommended coverage for the future value of money to take into account inflation.

- Use family expenses for calculation instead of personal expenses if you are the SOLE breadwinner of the family.

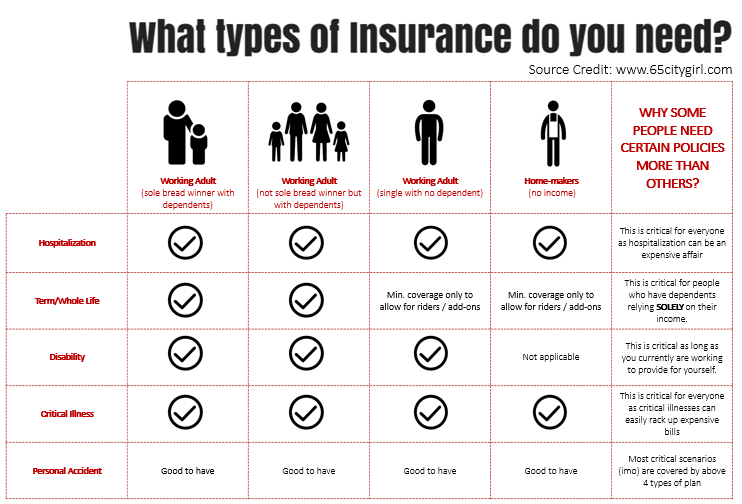

3) What kind of insurance should you buy?

Depending on the risks you foresee to impact you or your family the most, you should buy insurance to mitigate those risks accordingly. My personal view is to buy only what you need to protect yourself and your loved ones from financial risk so that you can spend the rest on savings and long-term retirement planning which should not be tied to insurance products.

What kind of insurance you need is typically dependent your individual working profile and family situation, so here are a few categories that people around the age 20-30+ would fall under:

As a female working adult who is not a sole bread winner but with dependents, I fall under the 2nd category where I have personally bought all 5 types of the insurance, yes I decided to be abit kiasu and get the Personal Accident plan too since it was really really cheap with reasonable coverage.

So what are the next steps you should take to buy the insurance you need?

So after reading up about the 3 simple points to explain:

- Why you need insurance?

- What type of insurances are available?

- What type of insurance is suitable for your needs?

What next? If you have no existing plans, I would suggest you start speaking to a trusted insurance advisor to go through details on coverage with you. If you have existing plans, having read this article do you think you are under or over covered, speak to your agent with these new information you have learnt and make suitable adjustments to your plans to suit your updated lifestyle needs.

I personally would recommend people speak to independent insurance advisors (who are agents not tied to any specific insurance firms) because they can help advise suitable products across different firms for your different needs. TRUST me, there is no ONE insurance firm that can provide the best product for ALL your needs. Luckily for me, I met a old friend who is an independent insurance advisor who helped me purchase and manage my policies across NTUC Income, Aviva and SOMPO.

I hope this short 10-15 minute read has helped to simplify some of your confusion on insurance policies and hopefully can kick start a more productive and focused conversation with your agents on YOUR needs not theirs.

For more comprehensive reading on insurance you can head over to DIY Insurance who have a portal of relatively updated information on various insurances. I am not affiliated to them in any way nor do I endorse their products, but I think their articles and information on the site are relatively helpful for people interested in reading up more to formulate their own opinions.